Neil Sinhababu and Nicholas Beaudrot's political blog

Wednesday, September 30, 2009

Tuesday, September 29, 2009

"Mostly Dead is Slightly Alive"

"Still Alive", "by" GLaDOS (hey, it was that or "Are You Dead Yet" by Children of Bodom. Trust me, this is the better choice).

Reactions seem to vary. If you want to be depressed, read Congress Matters or the Wonk Room. If you want to feel uplifted, Kos has a snippet of an interview with Tom Harkin or quotes from Health Care for America Now.

It's hard for me to read the tea leaves. Do the relevant players—Harry Reid, Nancy Pelosi, Chuck Schumer, Tom Harkin—have the stones to play hardball on the public option? Can the various moderates sustain their kabuki position of voting for cloture but against passage? How serious is their opposition? Hard to say.

My guess is that something like the Schumer amendment has 50 votes today, and Schumer is enough of a pragmatist that he may be able to mollify the remaining Senators to get past cloture vote (Bayh, Begich, Conrad, Lieberman, Lincoln, McCaskill, Ben Nelson, Pryor, Tester). And my guess is that that is something that most of the House progressives can live with. There will be a few no votes from the left: Kucinich, maybe Raul Grijalva, maybe Jim McDermott. But the center-left looks like it can hold.

Inching Forward

Chris Bowers and Steve Benen point out that the vote on a Schumer amendment—which includes a public option, but not one tied to Medicare rates—garnered the votes of Bill Nelson, and, somewhat shockingly, Tom Carper, which is probably a good sign for the prospects of an equivalent amendment on the floor. Indeed, Tom Harkin (D-IA) seems to "believe that there are, comfortably, 51 votes for a public option". It certainly looks that way, especially once someone tells to Kent Conrad that the Schumer plan looks nothing like the United Kingdom's health care system. Maybe TR Reid can give him a call and explain the thesis of his book one more time.

Now the question is, can the Leadership convince those Senators who are opposed to the public option not to join Republicans in a filibuster, and simply vote no for an amendment that passes the prospects for a serious bill are looking pretty good.

Now the question is, can the Leadership convince those Senators who are opposed to the public option not to join Republicans in a filibuster, and simply vote no for an amendment that passes the prospects for a serious bill are looking pretty good.

Eight Out of Thirteen

My stream failed during the roll call for Jay Rockefeller's public option amendment. This is the strongest of the bunch. It failed 8-15, and I was able to hear three "no" votes from Ds.

The Schumer and Schumer-Cantwell alternatives, which are not tied to Medicare, look much more promising from a political perspective. Nelson has announced he'll vote for Schumer-Cantwell, so we'll see how this goes.

- Kent Conrad

- Blanche Lincoln

- Max Baucus

The Schumer and Schumer-Cantwell alternatives, which are not tied to Medicare, look much more promising from a political perspective. Nelson has announced he'll vote for Schumer-Cantwell, so we'll see how this goes.

Roman Polanski

My understanding of the situation is that Roman Polanski made several good movies, and also raped a 13-year-old. The proper way for society to respond seems to be: admire his movies, and put him in prison for raping a 13-year-old. I don't really have a lot more to say about it.

Monday, September 28, 2009

If This Can Happen In Middle School, There's Hope For Humanity Yet

There's a sweet ending to this Amy Benfer post at Broadsheet about gay kids coming out at younger ages than before (sometimes in middle school). From the principal of an Los Angeles middle school with a thriving Gay Straight Alliance:

“And the most amazing thing has happened since the GSA started. Bullying of all kinds is way down. The GSA created this pervasive anti-bullying culture on campus that affects everyone.”You'd worry that middle school kids would just find something new to bully each other about, so that the total amount of bullying would remain constant. But no! Maybe sticking up for a group that is being bullied in a particularly visible way will generally disrupt the social structures within which bullying operates, causing kids to focus their energies on behaviors that are nicer and in all likelihood more fun. If this applies to the grownup world too, it would suggest that defending the rights of oppressed minorities can have a broad and beneficial social impact.

Sunday, September 27, 2009

XKCD Knows My Life

This was the story of my late teens and early 20s. (I wrote about it four years ago.)

Not that I didn't occasionally hit on girls in socially inappropriate ways (usually, because I had no idea what the rules were). But the number of times I did that is probably short of the number of times I now know somebody wanted to be a little more forward. Which means that there have got to be a whole bunch of unknown opportunities I passed up. And why did I pass them up? For exactly the reason the boy in the comic does. Because I was nervous that I'd be intruding on the girl's space or doing something creepy. I've learned some things over the years and gotten more confident, but I'm still that way a lot.

Not that I didn't occasionally hit on girls in socially inappropriate ways (usually, because I had no idea what the rules were). But the number of times I did that is probably short of the number of times I now know somebody wanted to be a little more forward. Which means that there have got to be a whole bunch of unknown opportunities I passed up. And why did I pass them up? For exactly the reason the boy in the comic does. Because I was nervous that I'd be intruding on the girl's space or doing something creepy. I've learned some things over the years and gotten more confident, but I'm still that way a lot.

Saturday, September 26, 2009

Nate Silver Vs. Strategic Vision

I'm watching this Nate Silver versus Strategic Vision thing with some interest. While I've been critical of Nate before, his quantitative goodness relative to broader media crappiness means I'd be quite happy to see him rise in stature. Helping to bring down a fraudulent pollster is the kind of thing that could be a real feather in his cap, so I'm hoping he's right.

I'm watching this Nate Silver versus Strategic Vision thing with some interest. While I've been critical of Nate before, his quantitative goodness relative to broader media crappiness means I'd be quite happy to see him rise in stature. Helping to bring down a fraudulent pollster is the kind of thing that could be a real feather in his cap, so I'm hoping he's right.On the actual issue at stake, I'd like to see more simulations that are comparable to Strategic Vision's polls. Nate has graphs up comparing the semi-randomness of the final digits in 2008 general election polling with the nonrandomness of the final digits in Strategic Vision's polling on everything. Those are useful, but something more than a pairwise comparison would probably help him make his case. It's hard to get an intuitive sense of how big an outlier Strategic Vision's results are in terms of the Benford's Law kinds of stuff if we only have one thing to compare them to.

Friday, September 25, 2009

Friday Obama Caption Contest

President Barack Obama talks with Indian Prime Minister Dr. Manmohan Singh during a G-20 leaders working dinner at the Phipps Conservatory and Botanical Gardens in Pittsburgh, Penn., Sept. 24, 2009. (Official White House Photo by Pete Souza).

President Barack Obama talks with Indian Prime Minister Dr. Manmohan Singh during a G-20 leaders working dinner at the Phipps Conservatory and Botanical Gardens in Pittsburgh, Penn., Sept. 24, 2009. (Official White House Photo by Pete Souza).

Debbie Stabenow Makes The Best "Your Mom" Comment In Human History

Jon Kyl (R-AZ): "I don't need maternity care...So requiring that on my insurance policy is something that I don't need and will make the policy more expensive."

Jon Kyl (R-AZ): "I don't need maternity care...So requiring that on my insurance policy is something that I don't need and will make the policy more expensive."Debbie Stabenow (D-MI): "I think your mom probably did."

This is why we need more women in the Senate. (And fewer idiots.) Jon Kyl can't be trusted to look out for his female constituents. This remark should be tied around his neck in 2012.

Thursday, September 24, 2009

How Well Did The AIDS Vaccine Work?

Lots of people were excited about the hopeful news from Thailand regarding an AIDS vaccine. Medical ethicist Udo Schuklenk, the co-editor of Bioethics, has a sobering reply -- the 31% reduction in rate of infection may just be an fluke result of low sample size. I don't know anywhere near enough about statistics to evaluate this issue myself, but I'll reprint his commentary:

The numbers seems to be speaking for themselves - 31%!!! - but do they? I doubt it. Here's the baseline as reported toward the end of the Los Angeles Times article: 'New infections occurred in 51 of the 8,197 given vaccine and in 74 of the 8,198 who received dummy shots. That worked out to a 31 percent lower risk of infection for the vaccine group.' The 23 additional infections in the placebo arm - out of 16400 overall participants - doesn't seem seem to be a figure that's statistically significant by any stretch of the imagination, no matter how hard the study's spin doctors (it cost 105 mio US$ to conduct the study) try to make it look otherwise. There might be good reason to undertake the same study with a much larger number of participants across the world, but until then, I doubt we have anything to celebrate at all.It'll be a month until the actual study is made public at a conference. Udo criticizes this as a case of "science by press release." His preferred strategy for dealing with AIDS is to put our resources into testing large numbers of people, and treating those who are infected.

For starters the number of people infected in both arms is fairly small (roughly 125 out of >16400, 51 in the active agent arm, 74 in the placebo arm - I doubt that is statistically significant, might be just a fluke).

Mathematical modelling suggests that the pandemic could be brought to heel within a generation or two by using this strategy. It turns out to be the case that this test-and-treat strategy is also the most efficient means to keep infected people alive and kicking. On my reading of the literature AIDS would turn from a terminal illness into a serious chronic illness that can be efficiently dealt with by means of medical care.

Blech

Well, I guess Nelson's "partially stick it to PhRMA by returning to 2003-law regarding dual-eligibles" amendment never had a chance. Baucus, Carper, and Menendez (D-BristolMeyersSquibb et al.) voted no, as did the only reachable Republican, Olympia Snowe. Nelson's amendment would have freed up $80 billion in revenue over the 10-year budget window, enough to completely close the donut hole in part D and still leave $30 billion for other purposes.

It's a travesty that costal state Dems like Menendez and Carper can't bring themselves to vote for this when interior moderates like Kent Conrad and Blanche Lincoln can. Yes, New Jersey is home to several large pharmaceutical firms, but it's also in the top quartile of spending per dual-eligible. Surely governor Corzine would be pleased to spend less and still get the same service.

It's a travesty that costal state Dems like Menendez and Carper can't bring themselves to vote for this when interior moderates like Kent Conrad and Blanche Lincoln can. Yes, New Jersey is home to several large pharmaceutical firms, but it's also in the top quartile of spending per dual-eligible. Surely governor Corzine would be pleased to spend less and still get the same service.

One-Half out of Five

In response to John Cornyn (R-TX) being obtuse, Max Baucus is describing some modest changes to regulations on employer-sponsored insurance. However, it only applies to new enrollees; that is, if you stay at the same company, the regulations don't apply to you.

This is news to me, and better than nothing. Still, it sucks. McDonald's can offer its employees "insurance" that's not as effectively regulated as something they can get in the exchange, and we're relying on employees to figure out that there's a better deal out there. Nonetheless, baby steps.

- First-dollar coverage

- Limits on annual out-of-pocket maxmimums

- No "unreasonable" annual or lifetime caps.

This is news to me, and better than nothing. Still, it sucks. McDonald's can offer its employees "insurance" that's not as effectively regulated as something they can get in the exchange, and we're relying on employees to figure out that there's a better deal out there. Nonetheless, baby steps.

Wednesday, September 23, 2009

Not a Snowe-Job

It's true that Olympia Snowe voted for a Republican amendment that would have stalled action on health care for a couple of weeks. But she's also been the only Republican to join Democrats on some amendments. One would have kept the overpriced Medicare Advantage plans alive, and another would have gutted MedPAC. Snowe's votes won't be perfect, but in the main, she's been on the side of the righteous much of the time.

Finance Committee Hearing Livetweeting

For the most part, my comments on this hearing are pretty short, so if for some reason you find what I have to say interesting, you're better off just following me on Twitter.

For the gluttons for punishment, you can watch the Finance Committee Hearing Live Webcast.

For the gluttons for punishment, you can watch the Finance Committee Hearing Live Webcast.

Tuesday, September 22, 2009

Bartender!

I just watched Tom Carper (D-DE) argue that the Senate should not vote to close the donut loophole for all seniors (44 million people) by returning the rate the government pays for drugs going to just to dual-eligible seniors (8 million people, mostly in nursing homes) to the rate paid prior to Bush's 2003 Medicare bill. Why? Because "we" made an agreement to limit Pharma's cuts to $80 billion, and it "wouldn't be fair" to go back on that agreement. Never mind that Tom Carper wasn't in the room when the agreement was made. Never mind that the existing donut hole is grossly unfair to seniors at or above the donut hole while accomplishing very little in terms of effective cost control (most recipients in the donut hole who can't afford the medicine just ... forgo the medicine rather than find some sort of magic plan). Never mind that sticking it to PhrMA is one of the bigger pots of money out there, and that other spending cuts are likely to involve lower-margin sectors such as hospitals, insurers (it's true! health insurance isn't as high margin), or providers. No, we can't push PhrMA further because that "wouldn't be fair".

I just watched Tom Carper (D-DE) argue that the Senate should not vote to close the donut loophole for all seniors (44 million people) by returning the rate the government pays for drugs going to just to dual-eligible seniors (8 million people, mostly in nursing homes) to the rate paid prior to Bush's 2003 Medicare bill. Why? Because "we" made an agreement to limit Pharma's cuts to $80 billion, and it "wouldn't be fair" to go back on that agreement. Never mind that Tom Carper wasn't in the room when the agreement was made. Never mind that the existing donut hole is grossly unfair to seniors at or above the donut hole while accomplishing very little in terms of effective cost control (most recipients in the donut hole who can't afford the medicine just ... forgo the medicine rather than find some sort of magic plan). Never mind that sticking it to PhrMA is one of the bigger pots of money out there, and that other spending cuts are likely to involve lower-margin sectors such as hospitals, insurers (it's true! health insurance isn't as high margin), or providers. No, we can't push PhrMA further because that "wouldn't be fair".If you'll excuse me, I'm going to retire to the warm embrace of some hard liquor.

For all the heat given to Max Baucus and Kent Conrad, Tom Carper was today's Wanker of the Day by a country mile. At least those two had the good sense to keep their mouths shut.

Voting starts on Wednesday at 9:30 am Eastern. Watch the gentleman from Delaware closely.

Finance Committee Markup Liveblogging

I'm listening to a laundry list recitation of changes to the Chairman's Mark. What can I say, I find this stuff interesting. You can get the full list from Senate Finance (PDF). For the most part, these changes incorporate amendments, or tweaked versions of amendments, offered by other Senators. Max Baucus seems to have incorporated every small-bore amendment Olympia Snowe asked for that has some positive value. But he's also incorporated a number of other amendments. In the main, the bill is now better. CHIP will be protected. Out-of-pocket maximums are lowered for everyone all they way up to 400% of FPL (very important!). The exchange is now opened to employees with up to 100 employees instead of 50. Tax changes will reduce the impact of the excise tax on expensive plans.

There are five big unsolved problems.

There are five big unsolved problems.

- The public option. We've still got these crappy co-ops. Funding for the co-ops has been boosted a little, but they're not really a Public Option By Another Name.

- Affordability. Baucus has cut premium maximums from 13% to 12% of income. Like I said, peanuts. We've really got to get down to 7-8% of income before we're in the realm of affordability. Ron Wyden is enlisting Doug Elmendorf to bring this point home; a middle-class household could still end up with out-of-pocket expenses close to 20% of income, when you include permiums and cost-sharing.

- Premium flexibility. The age variation has been lowered from 5:1 to 4:1. It should be 2:1.

- The free-rider provision. It's still there. It should be an employer mandate.

- Reforming the large-group/self-insured markets. Jay Rockefeller offered an amendment to force these markets to abide by the same reforms as the small-goup and individual markets. I thought I heard someone recite changes that would set some standards on employer-sponsored insurance, but I can't find it. There's a tension between the promise to let people keep what they have, and the promise to make insurance better overall, but at least in the long term the regulations ought to be harmonized.

Madonna & Justin Timberlake Tee It Up for Obama

He's only got four minutes to save the health care bill:

Scientific Psychology > Folk Psychology > Torture Excuse Psychology

Here's an obvious point given a haircut and dressed in a lab coat: if you waterboard people or put them under extremely stressful interrogations, you screw with their brain functioning so that they're much more likely to misremember things. It's now a paper in a psychology journal.

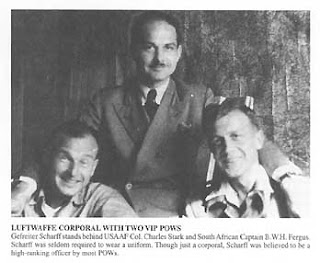

And that's still too generous to the interrogators. Ignorance of the relevant science is not at the root of the problems here. As the CIA knows, waterboarding produces false confessions, and that's what our interrogators were after. People with a serious interest in getting at the truth instead follow the path of Germany's best interrogator during WWII, Hanns Scharff, and befriend their prisoners so that they end up giving the best information they can of their own free will. Torture is what you get from Stalin's Russia or the Spanish Inquisition -- groups that aren't interested in the truth, but in confessions that make good propaganda. In our case, US interrogators were looking for a way to justify attacking Iraq.

And that's still too generous to the interrogators. Ignorance of the relevant science is not at the root of the problems here. As the CIA knows, waterboarding produces false confessions, and that's what our interrogators were after. People with a serious interest in getting at the truth instead follow the path of Germany's best interrogator during WWII, Hanns Scharff, and befriend their prisoners so that they end up giving the best information they can of their own free will. Torture is what you get from Stalin's Russia or the Spanish Inquisition -- groups that aren't interested in the truth, but in confessions that make good propaganda. In our case, US interrogators were looking for a way to justify attacking Iraq.

Just looking at the news article, the only disagreement I think I'd have with Shane O'Mara's paper is its claim that the torture methods were grounded in folk psychology of ordinary people rather than well-researched scientific psychology. Commonsense folk psychology tells you that people who want the torture to stop will say anything to end their pain, and that their confessions aren't going to guide you to the truth. Thomas Hobbes got this right a couple centuries before they built MRI machines:

The methods could even have caused the suspects to create — and believe — false memories, contends the paper, which scrutinizes the techniques used by the CIA under the Bush administration through the lens of neurobiology. It suggests the methods are actually counterproductive, no matter how much suspects might eventually say.

"Solid scientific evidence on how repeated and extreme stress and pain affect memory and executive functions (such as planning or forming intentions) suggests these techniques are unlikely to do anything other than the opposite of that intended by coercive or enhanced interrogation," according to the paper in the scientific journal Trends in Cognitive Sciences.

And that's still too generous to the interrogators. Ignorance of the relevant science is not at the root of the problems here. As the CIA knows, waterboarding produces false confessions, and that's what our interrogators were after. People with a serious interest in getting at the truth instead follow the path of Germany's best interrogator during WWII, Hanns Scharff, and befriend their prisoners so that they end up giving the best information they can of their own free will. Torture is what you get from Stalin's Russia or the Spanish Inquisition -- groups that aren't interested in the truth, but in confessions that make good propaganda. In our case, US interrogators were looking for a way to justify attacking Iraq.

And that's still too generous to the interrogators. Ignorance of the relevant science is not at the root of the problems here. As the CIA knows, waterboarding produces false confessions, and that's what our interrogators were after. People with a serious interest in getting at the truth instead follow the path of Germany's best interrogator during WWII, Hanns Scharff, and befriend their prisoners so that they end up giving the best information they can of their own free will. Torture is what you get from Stalin's Russia or the Spanish Inquisition -- groups that aren't interested in the truth, but in confessions that make good propaganda. In our case, US interrogators were looking for a way to justify attacking Iraq.Just looking at the news article, the only disagreement I think I'd have with Shane O'Mara's paper is its claim that the torture methods were grounded in folk psychology of ordinary people rather than well-researched scientific psychology. Commonsense folk psychology tells you that people who want the torture to stop will say anything to end their pain, and that their confessions aren't going to guide you to the truth. Thomas Hobbes got this right a couple centuries before they built MRI machines:

Also accusations upon torture are not to be reputed as testimonies. For torture is to be used but as means of conjecture, and light, in the further examination and search of truth: and what is in that case confessed tendeth to the ease of him that is tortured, not to the informing of the torturers, and therefore ought not to have the credit of a sufficient testimony.This isn't scientific psychology versus folk psychology. It's scientific psychology and folk psychology versus psychology designed to make excuses for torture.

Monday, September 21, 2009

The Awesomest Amendment Of Them All

Is clearly Hatch Amendment F7:

Is clearly Hatch Amendment F7:Short Title: Add transition relief for the excise tax on high cost insurance plans for any State with a name that begins with the letter “U.”Remember, kids, the Senate is a place for serious debate.

Baucus' Shifts The Mark

By tapping the $28 billion surplus for subsidies.

By tapping the $28 billion surplus for subsidies.In other words, Max Baucus has decided to throw the affordability crowd a few peanuts. Split evenly among the 31 million subsidized individuals in the exchange, over the five years that the exchange is operative, this would provide enough money to reduce premiums by $16/month per individual or about $32/month per family. Applied only to lower-income households, it barely provides enough revenue to get everyone between 133% and 150% of FPL down to Massachusetts-level premiums of $5-15/month. I don't think this will fool Jay Rockefeller. Update: The NYT has Baucus claiming this will be able to shrink premiums by 1% of income, which is $50 for a family of four at 300% of FPL (around $66,000 for a family of 4). We'd still need about four or five times that much money to make insurance truly affordable.

The bottom line continues to be that there's not enough revenue in the Baucus bill for insurance to be an affordable expense for anyone. You really need another $50-$60 billion/year to get premiums down to an affordable level. The best way to get that is by using existing health care dollars more efficiently, but the CBO doesn't want to score those savings. Applying the CAP failsafes to force the CBO to see some or all of those savings is the easiest way to save the largest amount of money. Combine that with Rockefeller's proposal to scale back itemized deductions, an increase on the excise tax on alcohol (which would improve public health and reduce crime) or start taxing Coke , and you probably have enough offsets to make things affordable.

(cc photo from Flickr user rachel is cocunut & lime).

Lord Help Me, I Disagree With Ezra on Something Regarding Health Care

I have a somewhat different take on some of Olympia Snowe's amendments than he does. For the most part he's almost certainly right. But there are a couple where I think may have missed the mark.

- The amendment to raise the maximum contribution to a tax-free FSA isn't a very good idea. FSA's are basically tax deductions for health care expenses that you get when you deposit the money into a special account, not when you file your taxes. But since they're deductions, rather than credits or refundable credits, they primarily benefit those who are already better-off; after all, you have to be able to save moeny to put in their FSAs, and working-class families usually don't save much. FSAs are also "use-it-or-lose-it", so you can't save your FSA deposits for a few years, and then use them to pay off your deductible when you end up in the hospital. Essnetially they are a way for the upper-middle class to pay for their co-payments and their kids' orthodontics with pre-tax dollars. There are much more urgent public policy priorities when it comes to health care.

- The amendment to cap deductibles doesn't help that much. As I read the amendment, it only caps deductibles, not the overall out-of-pocket maximum. The current maximum is simply too high, unless everyone between 133% and 300% of FPL gets subsidies here too (and I doubt they will, since then we'd have to subsidize household earning that much money who get their insurance through an employer, which is a ton of people). What you really need is to cap either the out-of-pocket maximum and/or raise the actuarial value of minimum creditable coverage. Several Democrats offered amendments to this effect.

Amendments That Matter

A number of Senators are out in full force to make the Finance Committee's final product suck less. Having spent quality time with almost 600 pages worth of PDF files, let me create some logical groupings of the Amendments.

Most of the important amendments in a cluster that most Democrats on the committee offered in some form or another. Most of these ought to pass.

As for Republicans not named Olympia Snowe, their amendments basically stink. Chuck Grassley (R-IA) co-sponsored one amendment for rural Medicare recipients that might have a bit of merit. The rest of them all blow, with one exception. The Baucus bill requires all insurers in the exchange to offer not just a bronze plan, but also silver and gold plans. At first blush, this requirement seems a little strange; why shouldn't we let some insurers offer only bronze plans? Might that result in more competition in at least part of the marketplace? I've had conversations with some actual health care wonks who think this is important, because otherwise the few companies that do offer silver and gold plans will get an unfairly high share of the high-cost patients. Perhaps you could fix this with risk-adjusted payments. But I don't know enough about the problem to say one way or another.

Now we'll have a week or two where we get to see which of the good ideas make it into the Finance Committee's bill. Considering this is the right-most pole of the debate, getting a bill out of committee with even a triggered public option, and something that pushes insurance into more affordable territory, would feel like a real win. It would mean that every Committee has produced something that's not particularly half-assed.

Most of the important amendments in a cluster that most Democrats on the committee offered in some form or another. Most of these ought to pass.

- The most common amendment is one to expand subsidies to 400% of FPL, and increase the level of subsidy in general. This one is a no-brainer. Baucuscare currently doesn't have enough money to make insurance affordable to anyone, and even the House bill leaves insurance close to unaffordable for millions of people it purports to help.

- Several Democrats are offering amendments to require self-insured businesses and large markets to abide by the same reforms that will apply in the exchange. For some reason, Baucus didn't apply the insurance market regulations that he created for the individual and small group market to large businesses that self-insure. So, your employer could still offer coverage that is less generous than the bronze coverage in the exchange. Fixing this is also a no-brainer.

- Next-most popular are amendments to scrap the co-ops in favor of a public option. This is a no-brainer, though, strictly speaking, there is such a thing as a good reform bill that doesn't have a public option.

- Following that in popularity are amendments that replace the free-rider with pay-or-play/employer mandate. The free-rider provision is quite simply the Worst. Policy. Ever. Kill it. Kill it dead.

- Next most popular were amendments to raise the minimum quality of insurance. Some of these limit the out-of-pocket maximums insurers can set in their products. Some of them increase the actuarial value of the plans. But in general, they force insurance plans to have less cost-shifting.

- Less popular, but vitally important, are amendments to narrow the rating band. The Baucus proposal allowed insurers tremendous variation based on age, smoking status, regions of the country, etc. Narrowing the band is absolutely vital. Yes, it will mean young people are cross-subsidizing the insurance of old people. But some day, the young people will be old, and they will be net winners rather than losers!

- Most Democrats want to ensure that stronger state regulations of insurance can continue to apply. The Baucus bill allows states to enter compacts to sell insurance across state lines. This sort of thing always results in a "race to the bottom" for the weakest insurance regulation, though Baucus's plan would have slowed that race. States with strong regulations could always decline to enter compacts with states that have weak insurance regulations. Still, the compact idea feels like a bad idea. But harmonizing regulations so that insurers don't have to deal with patchwork regulatory requirements might be a good idea. It seems to me that Baucus' idea could be made into some sort of grand bargain, where federal regulations preempt stronger state regulations, in exchange for which insurers accepts fairly stringent regulation, but it's not clear to me that anyone's interested in such a deal.

- A number of amendments were offered to improve state-level exchanges or the co-ops in one way or another, but it seems to me that having a national public option would be preferable anyway.

- It should be noted that most of the amendments offered by Ben Nelson and Blanche Lincoln tended to improve the bill. The worst amendments tended to come from Tom Carper (D-DE).

- A number of amendments are trying to improve insurance access for legal and/or illegal immigrants. These provisions are hard to parse, because they mostly have to do with who has the burden of proof and how annoying bureaucratic the appeals process is. At the very least, anyone ought to be able to purchase unsubsidized insurance in the exchange regardless of legal status.

- Jay Rockefeller has included amendments to restore living will counseling, which is a no-brainer and if our political system is worth four cents it will pass.

- There's a technical question of how to deal with CHIP, but I don't know what the best answer is. Rockefeller wants it out of the exchange. Others want it in the exchange, but with stricter cost-sharing rules. The point is, CHIP works and there's a lot of concern that this bill will blow up the existing CHIP programs.

- As far as paying for all of this, Jay Rockefeller's proposal is the best. He offsets almost all of his costs by limiting itemized deductions to 35% of income. This raises less revenue than the President's proposal (which I believe is to limit deductions to 28%), but the fact that Rockefeller says he's willing to do this means the idea isn't totally dead. Kerry wants to close corporate tax loopholes, which is also a salutary idea but of course raises the question of "whose loopholes are you gonna close?". Other ideas include increasing the tax rates on insurers drug companies, but I'm really a broad-base, low-rates kind of guy, so the Rockefeller proposal is the winner in my book.

- Olympia Snowe has her "trigger" amendment. The more I think about it, the more the trigger could be made to work. The main problem is that her threshold for the trigger is too high; 13% of income at 300% if FPL isn't really affordable insurance at all, but the idea is actually pretty sound.

- Snowe is also putting forth a collection of amendments to get this show on the road. Ezra points out that this is a very good idea; I'm going to be forty years old by the time the Baucus bill is fully implemented, which is just crazy. Massachusetts is close to full implementation within five years of passage.

- Ron Wyden has a number of bank-shot amendments that make final the bill look a bit more like Wyden-Bennett. For the most part these amendments are good policy but may be viewed as politically risky. In the main, they tear down the walls between the exchange and employer-sponsored insurance. In the long run, this is a very good idea. In the short run, it seems likely to scare people. If somehow, passing any of these amendments would convince Bill Bennett to vote for the final bill, (1) they would absolutely be worth passing, and (2) I will eat my hat.

- Kent Conrad cleverly offered a couple of amendments provide some immediate help in the small group/small business insurance market. This is good politics; the more immediate benefits people start to see, the happier they will be. However, Conrad, a self-proclaimed deficit hawk, couldn't be bothered to find offsets for his proposals.

- Blanche Lincoln put forth what appear to be a number of good amendments that made small changes. The one exception was an amendment to exempt "seasonal workers" from the headcount that determines who qualifies as a small business. Insuring farm workers seems like a genuinely tricky problem, and I don't know what to do about it. But outright excluding certain types of workers or employers strikes me as a bad idea.

- Democrats showed different degrees of enthusiasm for rolling back the tax exclusion for employer-provided health insurance or rolling back Baucus's excise tax on expensive insurance plans. Rockefeller wants the cap to be higher, so fewer health plans are hit by it (and less revenue is raised). Tom Carper wants it to be lower; in fact, he wants it to be only slightly higher than the national average cost of insurance, which is crazy low at this point in the debate. If anyone is in the right here, it's probably Rockefeller. Kerry's proposal is to set a different threshold for specific classes of businesses that are high risk (fisherman, miners, &c)

- John Kerry wants to let states create pilot programs that abandon fee-for-service. This is a very, very good idea that may be too hot to handle, but if the Senate's up to the task, we should do it. Suffice it to say I'm not holding my breath.

As for Republicans not named Olympia Snowe, their amendments basically stink. Chuck Grassley (R-IA) co-sponsored one amendment for rural Medicare recipients that might have a bit of merit. The rest of them all blow, with one exception. The Baucus bill requires all insurers in the exchange to offer not just a bronze plan, but also silver and gold plans. At first blush, this requirement seems a little strange; why shouldn't we let some insurers offer only bronze plans? Might that result in more competition in at least part of the marketplace? I've had conversations with some actual health care wonks who think this is important, because otherwise the few companies that do offer silver and gold plans will get an unfairly high share of the high-cost patients. Perhaps you could fix this with risk-adjusted payments. But I don't know enough about the problem to say one way or another.

Now we'll have a week or two where we get to see which of the good ideas make it into the Finance Committee's bill. Considering this is the right-most pole of the debate, getting a bill out of committee with even a triggered public option, and something that pushes insurance into more affordable territory, would feel like a real win. It would mean that every Committee has produced something that's not particularly half-assed.

Stanley McChrystal Requests Resources, As Managers Do

It's generally hard to know what to make of military commanders' requests for more resources. On one hand, they're very close to the situation at hand and thus have a very good knowledge of it. This fact gives them a great deal of credibility in public debate. On the other hand, they're managers, and managers always request more resources whether they need them or not.

It's generally hard to know what to make of military commanders' requests for more resources. On one hand, they're very close to the situation at hand and thus have a very good knowledge of it. This fact gives them a great deal of credibility in public debate. On the other hand, they're managers, and managers always request more resources whether they need them or not.This second fact isn't that well appreciated in media coverage of their requests, but it's something that anybody who works in a big organization is very familiar with. If you went to Sor-Hoon Tan, my department chair, and asked her if she'd like to have funds to hire two more philosophy professors, she'd say yes. As would the chair of just about every department in the country. Nobody ever says, "Well, we're making great use of what we have, and while we could do more work with more resources, these positions would really be put to better use in Sociology, so why don't you give this money to them." When something is your job, you focus on doing it, whether it's building the NUS philosophy department or rooting out the Taliban in Afghanistan. Whether the resources you're requesting could be put to better use elsewhere is far from your mind.

It's especially true in a context where there aren't strict metrics for efficient performance and you're going to be evaluated primarily on whether the job gets done, not on how efficient you were with what they gave you. Nobody is going to evaluate McChrystal on whether he accomplished more per life lost or dollar spent than say, Norman Schwarzkopf in the Gulf War, because we don't have any metrics for stuff like that. In fact, requesting resources that can't be used efficiently is probably in McChrystal's interests. The more resources we push into Afghanistan, the bigger a deal Afghanistan is. And the bigger a deal Afghanistan is, the bigger a deal he is if we win. If he pulls it out after making everything look dire, so much the better.

This isn't to accuse the general of doing anything corrupt or particularly self-serving. He's just following the incentives that our system gives him, and that everybody in a position like his pursues. What would be particularly corrupt is if he, say, left his command for a cushy job at some company that profited from his resource requests. (I don't know if generals do that often, though members of Congress certainly do it. Billy Tauzin's name probably deserves to be turned into a word for this.)

There are a lot of ways in which military spending escapes the scrutiny that's applied to domestic budget requests, and this is one of them. If Kathleen Sebelius came out tomorrow and said that the medical and economic situation of ordinary Americans required a health care plan that went above the $1 trillion mark over ten years, it wouldn't have nearly the impact of McChrystal's letter today. Nobody out there has the clout to make the kind of demands on the system that generals do, and they're always going to be demanding more.

Sunday, September 20, 2009

I Bet She Clogs Your Friends Feed With Annoying Quizzes

Lots of people on Facebook, including myself, use the site as a means for expressing their political views. Many of us probably think it would be a pretty awesome thing to be an elected official and wield real power. But since we aren't in that position, we try to communicate their views to others by putting up occasional witty/informative status updates and so forth.

It looks like Sarah Palin left the governorship of Alaska to become one of us hapless people on Facebook. This is a medium where nobody can make Sarah Palin answer difficult questions like "What newspapers do you read?" Or at least, if you post that on her wall, she can delete it and de-friend you.

It looks like Sarah Palin left the governorship of Alaska to become one of us hapless people on Facebook. This is a medium where nobody can make Sarah Palin answer difficult questions like "What newspapers do you read?" Or at least, if you post that on her wall, she can delete it and de-friend you.

Saturday, September 19, 2009

Condoms Will Save The World, If Only We Let Them

According to a new study from the London School of Economics, eliminating unwanted pregnancies through family planning and contraception is four to five times more cost-effective than rolling out low-carbon technologies. Preventing unwanted pregancies (and the resulting overpopulation, which results in more environmental destruction and global warming) costs $7 per ton of carbon. Low-carbon energy sources go from wind at $24 per ton on up, for an average of $32 per ton.

According to a new study from the London School of Economics, eliminating unwanted pregnancies through family planning and contraception is four to five times more cost-effective than rolling out low-carbon technologies. Preventing unwanted pregancies (and the resulting overpopulation, which results in more environmental destruction and global warming) costs $7 per ton of carbon. Low-carbon energy sources go from wind at $24 per ton on up, for an average of $32 per ton. Unfortunately, as Lydia DePillis notes, the Sierra Club and the Obama Administration are too nervous to talk about this, because family planning is controversial. Hurts to type that.

Friday, September 18, 2009

Super-Size The House!

I'm not sure that this legal challenge is going to get anywhere, but it does highlight an important point. In addition to the fact that our relatively small legislature means that most Representatives have too many constituents, the system modestly disenfranchises voters who happen to live in districts that are not quite large enough to be split in two. Montana, for instance, has 80% more residents than Wyoming, but both states have exactly one Representative.

One question is whether such a system would tend to strengthen or weaken party discipline. That's harder to know. However, considering the fact that most parliamentary democracies have minor parties that occupy a few seats, one might expect that in America's two-party system, factions would form that replicated the effects of minor parties. To an extent, we already have this today, with the Progressive Caucus, the Republican Study Committee, the Congressional Black Caucus, and so forth.

One question is whether such a system would tend to strengthen or weaken party discipline. That's harder to know. However, considering the fact that most parliamentary democracies have minor parties that occupy a few seats, one might expect that in America's two-party system, factions would form that replicated the effects of minor parties. To an extent, we already have this today, with the Progressive Caucus, the Republican Study Committee, the Congressional Black Caucus, and so forth.

Friday Obama Caption Contest

Actual caption: "First Lady Michelle Obama and President Barack Obama meet with the Crown Prince and Princess of the Netherlands in the Yellow Oval Room of the White House in Washington, D.C., Sept. 11, 2009. (Official White House Photo by Samantha Appleton)".

Actual caption: "First Lady Michelle Obama and President Barack Obama meet with the Crown Prince and Princess of the Netherlands in the Yellow Oval Room of the White House in Washington, D.C., Sept. 11, 2009. (Official White House Photo by Samantha Appleton)".Leave your caption in the comments. Bonus points for funny captions that don't reference either weed or Pulp Fiction. Though, don't let that stop you from making Pulp Fiction-related jokes ... they're funny!

No Subtext Here. Nope, None Whatsoever

There are lots of crackpots in the Republican Party. But you don't see aides dishing backbiting quotes in The Politico trashing any of them. Mr. Steve King doesn't get this treatment. Nor do the various cranks from Georgia or Texas, Mr. Tom m Price, Mr. Paul Broun, Mr. Lynn Westmoreland, Mr. Jack Kingston, Mr. Louie Gohmert, etc., despite the fact they've all said a number of equally boneheaded things. But Ms Michelle Bachmann is apparently subjected to a different standard.

It's true, there's something different about Michelle Bachmann's crankery. I wonder what that could be.

It's true, there's something different about Michelle Bachmann's crankery. I wonder what that could be.

Thursday, September 17, 2009

What Sir Charles Said

This has been another edition of what Sir Charles said. Most people won't care if the health care bill is deficit neutral, or if it has a public option, or really any number of things. For most voters, the main issue with health care reform is that it has to not suck. And that means it has to be within the realm of affordability and providing insurance that's actually worth a darn. Which the current bill doesn't do, at all.

At this point, unless there's some magical set of revenue or spending offsets out there that I'm not aware of, I'm tempted to say we should eliminate the mandate, up Medicaid payments and cover everyone up to 200% of FPL, cover children up to 400% of FPL, and call of the day. Telling 25 million people they have to take out another substantial expense without getting much value for it isn't going to fly.

At this point, unless there's some magical set of revenue or spending offsets out there that I'm not aware of, I'm tempted to say we should eliminate the mandate, up Medicaid payments and cover everyone up to 200% of FPL, cover children up to 400% of FPL, and call of the day. Telling 25 million people they have to take out another substantial expense without getting much value for it isn't going to fly.

Why Massachusetts Worked (relatively) Well

After reading through the transcript of a Kaiser panel on the Massachusetts reform, it bears repeating that Massachusetts had several things going for it that made

- In the 1990s, the state had enacted tax increases to compensate providers for charity care. Thus there was already a substantial pot of money that could be redirected.

- Prior to reform, the state had a fairly low level of uninsured (10% versus about 15% nationwide)

- The state is relatively prosperous.

- The state has a strong culture of civic responsibility, which lessened business community opposition to reform, and robust civic culture, which means there were lots of people who could help with community outreach into areas with a large number of uninsured.

Wednesday, September 16, 2009

Baucuscare and Affordability Alternatives: Yes We Can!

As you're reading this, keep in mind, I'm doing serious back-of-the-envelope math. I'm not the CBO. I don't study health economics for a living. I make bone-headed errors because it's just me and it's easy to forget when you need to divide by two. The professionals at CBO, or CAP, or the Kaiser Family Foundation, or the Kennedy School, or wherever David Cutler works, or any number of other places can give you a much more accurate estimates of the effects of this or that reform. But the numbers are easy enough to work with that we can at least get good ballpark estimates of which ideas are good, and which ideas are a waste of time; provided, of course, that we remember when to divide by two.

But the back of my envelope has some surprisingly good news. You can get a bipartisan bill that's more affordable than the Massachusetts system with three changes:

I'm surprised at how easy this turned out. At some level, it feels too good to be true. Most likely, there are large political obstacles to implementing the CAP proposal. Perhaps it will anger AARP. Maybe it will anger the AMA. Maybe it will anger large teaching hospitals, which tend to be in urban districts represented by Democrats. Maybe these reforms would require taking "Medicare" dollars and using them to pay for something else, which is a big no-no. I'm not close enough to The Hill to understand the political calculus. But from an accounting standpoint, it seems like a no-brainer. I'm vaguely hoping that someone can prove me wrong, because I'm pretty sure health reform isn't supposed to be this easy.

So let's see how this works.

Warning: long and gory details to follow.

In the previous post in this series, we saw that Baucuscare isn't quite affordable enough. This is why people like Ron Wyden keep saying things like "it's very clear, at this point in the debate, the flashpoint is all about affordability". The Massachusetts plan, which is popular, has significantly lower monthly payments than the proposed Baucus plan. In fact, even if we were to use the levels of funding in the House bill, there still isn't enough money to get everyone within shouting distance of premium payments in Massachusetts. We can get acceptably low payments for everyone up to 200% of FPL, but that leaves very little money to help the eight million Americans earning 200%-300% of FPL. To get these households to monthly payments near those seen in Massachusetts would require $22 billion per year in additional subsidies, bringing the ten-year cost of the bill to about $1.15 trillion or higher (remember, a lot of this stuff doesn't go into effect until 2013) What else can be done? There are five major levers the government can pull to bring the cost of insurance. Well, okay, there are six—we could just move to single-payer. But, sadly, setting that one aside, there are five options.

But the back of my envelope has some surprisingly good news. You can get a bipartisan bill that's more affordable than the Massachusetts system with three changes:

- Putting failsafe spending cuts and revenue increases alongside cost-control measures (IMAC, health IT adoption, etc.) as CAP recommends.

- Plowing all the savings from (1) into more generous premium subsidies.

- Convincing Olympia Snowe that this is a good idea.

I'm surprised at how easy this turned out. At some level, it feels too good to be true. Most likely, there are large political obstacles to implementing the CAP proposal. Perhaps it will anger AARP. Maybe it will anger the AMA. Maybe it will anger large teaching hospitals, which tend to be in urban districts represented by Democrats. Maybe these reforms would require taking "Medicare" dollars and using them to pay for something else, which is a big no-no. I'm not close enough to The Hill to understand the political calculus. But from an accounting standpoint, it seems like a no-brainer. I'm vaguely hoping that someone can prove me wrong, because I'm pretty sure health reform isn't supposed to be this easy.

So let's see how this works.

Warning: long and gory details to follow.

In the previous post in this series, we saw that Baucuscare isn't quite affordable enough. This is why people like Ron Wyden keep saying things like "it's very clear, at this point in the debate, the flashpoint is all about affordability". The Massachusetts plan, which is popular, has significantly lower monthly payments than the proposed Baucus plan. In fact, even if we were to use the levels of funding in the House bill, there still isn't enough money to get everyone within shouting distance of premium payments in Massachusetts. We can get acceptably low payments for everyone up to 200% of FPL, but that leaves very little money to help the eight million Americans earning 200%-300% of FPL. To get these households to monthly payments near those seen in Massachusetts would require $22 billion per year in additional subsidies, bringing the ten-year cost of the bill to about $1.15 trillion or higher (remember, a lot of this stuff doesn't go into effect until 2013) What else can be done? There are five major levers the government can pull to bring the cost of insurance. Well, okay, there are six—we could just move to single-payer. But, sadly, setting that one aside, there are five options.

- Make the employer mandate real. The Baucus bill doesn't have an employer mandate or pay-or-play rule. Instead, it has the Worst Idea Ever. This is a shame, because employer mandates seem to increase the number of people using employer-provided insurance, even with a seemingly small penalty. In Massachusetts, the pay-or-play provisions induced employers to provide insurance to about 20% of the uninsured. Some employers started offering insurance. More importantly, a number of middle-class or "young invincible" individuals who currently decline insurance to get a few extra bucks in their paycheck started using their employer's insurance plan. If we ended up with the same results nationwide, the individual insurance market would shrink from 46 million to 37 million. However, it's difficult to estimate how this would impact the government's ability to provide premium subsidies. It would depend greatly on the income levels of the people who left the individual market and bought insurance through their employer. If 15% of households earning 133-200% of FPL bought insurance through an employer, 20% between 200% and 300%, and 30% above 300%, the smaller pool in the subsidized individual market, monthly subsidies would increase by about $20 per person, or $75 for middle-class family of four if we start from the "House+low-income tilt" baseline.

- Expand Medicaid to 150% or 167% of FPL. Medicaid pays slightly less per enrollee than the cost of individual insurance, while offering lower co-payments and deductibles. Of course, the low payments are one reason providers tend to dislike Medicaid. Still, if you mitigated provider opposition by increasing Medicaid payouts from adults from its current level of $2150/enrollee to $2400/enrollee, you would still spend slightly less money and get slightly more health services. You'd also shrink the pool of uninsured by at least 5 million, leaving fewer people who will need subsidized insurance. At best, though, this would increase the subsidy level by another $25-30 per person, or $90 for a family of four using the "House funding+low-income tilt" baseline.

- Stick it to the drug companies. Congress could choose to ignore Barack Obama's secret deal with PhRMA that may or may not exist. That agreement reduced the government's 10-year cost for prescription drugs by $80 billion. Nancy Pelosi and others have suggested there's another $80 billion on the table. Plowing those savings into subsidies would reduce premiums by about $50/month per individual, or, if we use the House scenario tilted towards low income spending, would reduce premiums for a family of four between 200% and 300% of FPL by another $160/month (in this scenario premiums for working-class households are already at acceptable levels).

- Give SCHIP to more children. Children are relatively cheap to ensure; nationwide, spending per SCHIP enrollee is roughly $1700 per year. In addition, 69% of uninsured children are in households earning less than 200% of FPL, compared to 66% of the total population. Therefore insuring children through SCHIP is modestly progressive; it will do more for working-class and poor households than it will do for the middle class, even if they all receive full coverage. Insuring middle-class children through S-CHIP would also enable their parents to purchase individual or individual+spouse plans instead of full family plans. That would cut premiums by $200-250 per month. However, S-CHIP expansion provide no benefit to singles, nor to couples without children. Parents and children account for only half the uninsured population, so only half of those on the individual market would see any benefit.

In Massachusetts, all children in households earning less than 300% of FPL are fully covered. You can afford to do adopt this policy nationwide and still enough money left over to provide decent subsidies to adults in the 200%-300% FPL range. - Hope the CBO is wrong. Much ink has been spilled over the question of whether or not the CBO is being too conservative in calculating how much impact the cost-cutting measures will have. Perhaps they will be proven wrong. But hope is not a plan. One solution to this is CAP's proposal to include failsafe policy changes that force cost cutting or tax increases in the event that savings don't materialize. This would allow the CBO to "see" the savings that we expect IMAC and other reforms will realize. This would almost certainly make enough difference in the scoring of the bill, since the Cutler/Feder paper estimates that there are $580 billion in savings on the table. That's huge. It's enough to get Baucuscare into the realm of affordability all on its own; we could provide premiums equal to what Massachusetts provides and still have money left over to subsidize insurance between 300% and 400% of FPL.

- Adopt failsafe spending cuts & tax increase in the event IMAC can't deliver cost control

- Boost funding from Baucus levels ($850B) to House levels ($1.04T)

- Expand full SCHIP coverage to 300% of FPL, with partial coverage up to 400% of FPL.

- Play hardball with PhRMA

- Expand Medicaid eligibility

- Make the employer mandate real

Baucus Wonders: Not Making Filing Taxes Worse

I was prepared to write a long screed about how all the proposals to subsidize health insurance involve issuing tax credits, which would make filing taxes more complicated and tie government mandated health insurance to everyone's least favorite day of the year. Thankfully, Baucuscare breaks this link. While people will have to keep their tax forms to apply for insurance, the credit will be issued at the time of the insurance application, not on April 15th. That's goodness that should be imported into the final bill.

The rest of the bill .... well, it has its moments.

The rest of the bill .... well, it has its moments.

In Defense Of The (Second) Bag Fee

I've done a fair bit of travel over the past month. I think I can report that at the margin, bag fees on the first bag encourage two behaviors:

- Travelers pack the largest bag they think they can carry on to the plane. This results in higher boarding and de-planing times as they struggle to put their bags in overhead compartments. In addition, nearly every flight on airlines that charge for the first bag has less than zero space for carry-on luggage; they know that there are more bags than there are overhead compartments-plus-space-under-seats. This is the bottleneck for airline to earn more revenue; if they could shrink boarding times by ten percent and get an extra flight out of each plane, they'd be very happy. So at this level, the fee for the first bag is penny-wise and pound-foolish.

- Travelers pack a large bag and expect the flight attendants to deny them the chance to carry it on. But, they don't (can't?) charge you for bags they force you to check at the gate. As more and more people figure this out, it will become the norm, and airlines will either be forced to abandon the fee for the first bag, or start charging people at the gate, which means they'll have to start charging you for checking the stroller, which means the airlines hate children, Congress will intervene, &c.

Baucus Blunders, Part II: Affordability

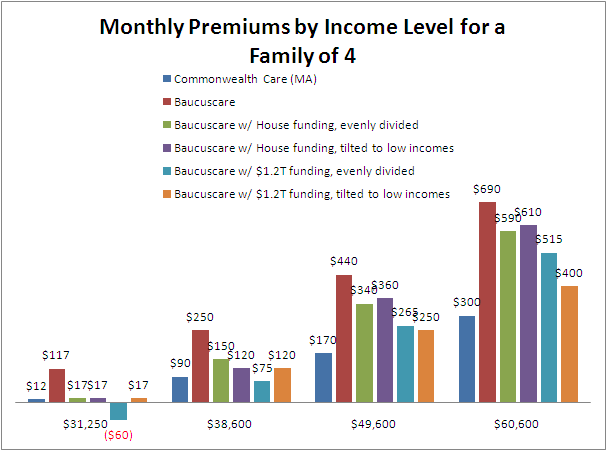

Facepalm update: Oh dear. I've made a terrible error in calculating premiums under alternative scenarios; I've assumed everyone in every income bracket is buying a family based policy. This is wrong, and because of the way I calculated premiums, it means that the "Baucuscare, w/House funding ..." alternative scenarios have higher premiums for those earning 200%-300% of FPL than they actually would under those scenarios. Instead of $90/month in higher subsidies, a family of four would see at least $290 in higher subsidies with $1.2T of funding. Still, even with these adjustments, which are now reflected in the chart, the House alternatives are noticeably more expensive than the Massachusetts plan. Funding above and beyond the $1.04 trillion that HR 3200 contemplates still doesn't get subsidies to Massachusetts levels.

First, let's list the people who will be much better off under Baucuscare than they currently are. Remember, keep the flowchart in mind:

[The income levels here, by the way, are 141%, 175%, 225%, and 275% of FPL; essentially the midpoint of each income bracket]

[The income levels here, by the way, are 141%, 175%, 225%, and 275% of FPL; essentially the midpoint of each income bracket]

People in Massaschusetts are by and large satisfied with the Connector. It's toughest on the fairly small number of families earning just over 300% of FPL (of which there aren't that many), and on the larger number of young individuals who make just over 300% of FPL (which is $32,320 for an individual, so there are a decent number of those folks). Working class families earning up to 200% of FPL have fairly low premiums. $90 per month is going to pinch, but for uninsured households, they'll get some real value out of that: Commonwealth Care plans include dental insurance, wellness checkups have low co-payments; chronic disease care is especially well covered, and so forth. Likewise, three hundred pre-tax dollars a month for a family with a gross income of $60,000 per year is Real Money, but it's not going to break the bank. It's less than what they should be saving for college, for instance.

But as you can see from the graph, the Baucus bill doesn't fare as well. It's not even close to faring as well. The eight million individuals without insurance who earn between 200% and 300% of FPL will pay more than twice what similar households in Massachusetts currently pay. And working class families will feel a real pinch; $250 per month ($3,000 per year) for a family of four with an income of $38,000 is going to hurt. (This paragraph was edited for clarity)

The alternative scenarios are not quite as bad. I especially like thepurple orange scenario, using funding levels higher than the House bill to push premiums down primarily for working-class households. That would be almost as good as what Massachusetts has. And politically it would probably be fairly popular.

Up next: I'll explore policy options to get the red bar closer to the dark blue bar. Who said charts weren't fun?

First, let's list the people who will be much better off under Baucuscare than they currently are. Remember, keep the flowchart in mind:

- New Medicaid qualifiers who are currently uninsured. These are the 14 million people who earn less than 133% of FPL ($29,300 for a family of 4) who will now qualify for Medicaid. This is a huge boost to their well-being and financial security. In fact, individuals between 100% and 133% of FPL are better off under Baucuscare than they would be under the Massachusetts plan, since Medicaid has less cost sharing than Commonwealth care.

- Working and middle-class households who buy individual insurance policies. These are the six million people between 133% and 300% of FPL who currently buy individual insurance policies on the private market. They will now pay less for insurance. Or they will pay the same amount, but they will have better insurance. Baucuscare is good for these people.

[The income levels here, by the way, are 141%, 175%, 225%, and 275% of FPL; essentially the midpoint of each income bracket]People in Massaschusetts are by and large satisfied with the Connector. It's toughest on the fairly small number of families earning just over 300% of FPL (of which there aren't that many), and on the larger number of young individuals who make just over 300% of FPL (which is $32,320 for an individual, so there are a decent number of those folks). Working class families earning up to 200% of FPL have fairly low premiums. $90 per month is going to pinch, but for uninsured households, they'll get some real value out of that: Commonwealth Care plans include dental insurance, wellness checkups have low co-payments; chronic disease care is especially well covered, and so forth. Likewise, three hundred pre-tax dollars a month for a family with a gross income of $60,000 per year is Real Money, but it's not going to break the bank. It's less than what they should be saving for college, for instance.

But as you can see from the graph, the Baucus bill doesn't fare as well. It's not even close to faring as well. The eight million individuals without insurance who earn between 200% and 300% of FPL will pay more than twice what similar households in Massachusetts currently pay. And working class families will feel a real pinch; $250 per month ($3,000 per year) for a family of four with an income of $38,000 is going to hurt. (This paragraph was edited for clarity)

The alternative scenarios are not quite as bad. I especially like the

Up next: I'll explore policy options to get the red bar closer to the dark blue bar. Who said charts weren't fun?

Tuesday, September 15, 2009

Deep Thought

Remember when Terry Moran leaked George Bush's off the record comments about the Jeremy Shockey's homophobic outburst?

Yeah, me neither.

Yeah, me neither.

Baucuscare Blunders, Part I: Pricing for the Middle Class

Update: thinking about this a bit more, the fact that health care expenditures are deductible makes Baucus care somewhat less expensive than this chart suggests. Depending on the effective income tax burden of a family making $66,000, Baucuscare may be less expensive than Catholic school or even a car. Still, it's a major new expense.

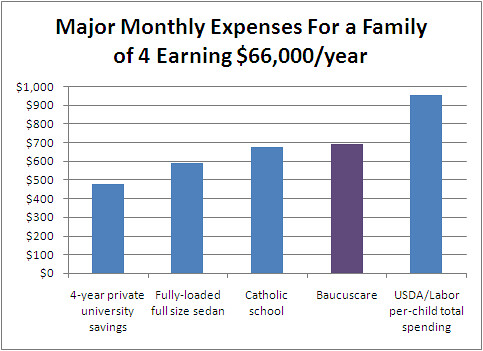

I've previously argued that we should think about the out-of-pocket expenses for health insurance relative to other major expenses facing the middle class. So, now that Jon Cohn has tracked down a spreadsheet making the rounds among Baucus' acolytes, let's do some comparisons. Remember, we're thinking of a family of four—two adults and two children—with a pre-tax household income of $66,000 that is currently uninsured, keeping in mind that most households with this income level already have insurance:

And for the visual learners out there:

So, there you have it: for middle-income households that currently don't have insurance (roughly 12 million people between 200% and 400% of FPL) insuring the entire family will slightly more expensive than saving for a child's college years. It will be about the same price as owning another fairly nice car (once you consider gas & insurance costs), or sending a kid to Catholic school. And it will be slightly less expensive than having another child. These are things middle-income households currently do; they may not do all of them, but they frequently do at least one. If Baucuscare passes as currently written, it will add another major expense for uninsured middle income households (did I mention, most people at this income level already have insurance)?

This will have a real impact on American society. Fewer people will declare bankruptcy because of health care expenses. But several million middle-income Americans will now be less likely to buy fully-loaded Toyota Camrys and more likely to buy zero-options Subaru Outbacks. Or they will live in somewhat smaller homes. Or they will spend lots of time thinking about how to live in a decently priced neighborhood with decent public schools rather than send their children to Catholic school. More parents will ask their teenage children to hold down jobs to help save money for college, end up with kids who have more student loans, or simply not send their children to college at all. More families will decide to have one child instead of two, or two instead of three.

Since I've repeated several times the fact that most people at this income level already have insurance, it's worth pointing out that people at this income level already buying insurance on the private individual market will be made better off by Baucuscare. They will suddenly find themselves paying less for insurance. Or they will pay the same amount, but they will have better insurance. Between 300% and 400% of poverty, there are as many people on the private nongroup market as there are who are uninsured. Between 200% and 300% of FPL, three times as many are uninsured as are in the private nongroup market.

Coming next: how Baucuscare compares to Romney care on affordability. Hint: not well.

I've previously argued that we should think about the out-of-pocket expenses for health insurance relative to other major expenses facing the middle class. So, now that Jon Cohn has tracked down a spreadsheet making the rounds among Baucus' acolytes, let's do some comparisons. Remember, we're thinking of a family of four—two adults and two children—with a pre-tax household income of $66,000 that is currently uninsured, keeping in mind that most households with this income level already have insurance:

- Monthly savings required to cover average net cost of 4-year private university expenses, starting from birth: $475/month

- Fully-loaded Honda Accord or Toyota Camry, 7% interest over 5 years: $575-600/month

- Average tuition at a Catholic school: $675/month

- Baucuscare for a family of four: $700/month

- USDA/DOL estimate per-child spending for middle-income households: $800-1100/month

And for the visual learners out there:

So, there you have it: for middle-income households that currently don't have insurance (roughly 12 million people between 200% and 400% of FPL) insuring the entire family will slightly more expensive than saving for a child's college years. It will be about the same price as owning another fairly nice car (once you consider gas & insurance costs), or sending a kid to Catholic school. And it will be slightly less expensive than having another child. These are things middle-income households currently do; they may not do all of them, but they frequently do at least one. If Baucuscare passes as currently written, it will add another major expense for uninsured middle income households (did I mention, most people at this income level already have insurance)?

This will have a real impact on American society. Fewer people will declare bankruptcy because of health care expenses. But several million middle-income Americans will now be less likely to buy fully-loaded Toyota Camrys and more likely to buy zero-options Subaru Outbacks. Or they will live in somewhat smaller homes. Or they will spend lots of time thinking about how to live in a decently priced neighborhood with decent public schools rather than send their children to Catholic school. More parents will ask their teenage children to hold down jobs to help save money for college, end up with kids who have more student loans, or simply not send their children to college at all. More families will decide to have one child instead of two, or two instead of three.

Since I've repeated several times the fact that most people at this income level already have insurance, it's worth pointing out that people at this income level already buying insurance on the private individual market will be made better off by Baucuscare. They will suddenly find themselves paying less for insurance. Or they will pay the same amount, but they will have better insurance. Between 300% and 400% of poverty, there are as many people on the private nongroup market as there are who are uninsured. Between 200% and 300% of FPL, three times as many are uninsured as are in the private nongroup market.

Coming next: how Baucuscare compares to Romney care on affordability. Hint: not well.

Once Again, Returning to The Flowchart...

Electorally, setting the cap at 300% versus 400% of the Federal Poverty Level isn't a big deal. Roughly four million Americans—people, not households—are currently uninsured and have household incomes between 300% and 400% of FPL. These are households that will suddenly find themselves with a government mandated expense that's going to pinch them at some point in the next five years. Most people at that income bracket have employer-provided insurance; those that do not frequently purchase insurance on the individual market. By comparison, 44 million seniors will immediately see the donut hole in out-of-pocket prescription drug expenses shrink in half. Do I think that the subsidy level ought to reach higher than 300%? Yes, particularly because people earning 250% of FPL are going to need more help than the bill currently provides. Do I think leaving the subsidy level at 300% will lead to electoral disaster? No.

Makin' Memories At The Pottery Wheel, Rubbin' Clay On You All Afternoon

Matt is blogging about a twitter conversation between foreign policy people (what has the world come to?) about how to define victory in Afghanistan, and it's seeming like Obama has a big advantage on his side regarding the domestic politics of Afghanistan. The question of what constitutes victory has gotten so unclear and popular American understandings of the situation on the ground are so murky that any definition of victory confidently presented by a reasonably popular administration will be accepted.

So if Obama wants to set the bar really low, hop over it, and go home, he can do that and look like a winner. Maybe the easy goal is making sure the Taliban don't rule Afghanistan again or something like that. Or if he sees a well-defined, worthwhile, and potentially achievable goal that's a little more difficult, he can pursue that. But I hope he realizes that he's got control over the definition of victory, at least as far as American perceptions are concerned, and he can use that as he wants.

So if Obama wants to set the bar really low, hop over it, and go home, he can do that and look like a winner. Maybe the easy goal is making sure the Taliban don't rule Afghanistan again or something like that. Or if he sees a well-defined, worthwhile, and potentially achievable goal that's a little more difficult, he can pursue that. But I hope he realizes that he's got control over the definition of victory, at least as far as American perceptions are concerned, and he can use that as he wants.

Monday, September 14, 2009

Dig a Pony

Life converges in strange ways. A song with this title is included The Beatles: Rock Band. Weird.

Not being familiar with the band's back catalog, this was news to me. Perhaps John McCain had some sort of subconscious inspiration when he used the phrase.

Not being familiar with the band's back catalog, this was news to me. Perhaps John McCain had some sort of subconscious inspiration when he used the phrase.

Yet More On Walking To School

Amanda Marcotte observes that while the chances of a child being assaulted is quite low, the chance of pretty much anyone with two X chromosomes being subject to catcalls is absurdly high. The standard prescription is to make sure kids walk around in groups of mixed gender wherever possible, but obviously that's not practical all of the time, nor does it always work. Nonetheless, as she also points out, mothers do the lion's share of child-rearing in the overwhelming majority of two-parent American households. Therefore social norms that tend to increase the amount of child-rearing will tend to eat more into womens's free time than men's.

All these things are true, and I'm not really big on moralizing over other people's parenting decisions. People can draw their own conclusions from the data.

All these things are true, and I'm not really big on moralizing over other people's parenting decisions. People can draw their own conclusions from the data.

Afghan Soldiers Can't Read

I don't really know what point to make with this, but apparently 9 out of 10 soldiers in the Afghan National Army can't read. Here's one guy: